Alphabet Inc. (GOOGL)-Focused Growth 12 - Metric System Review

Alphabet Inc. (GOOGL) remains one of the largest and most dominant companies in the tech sector. This review uses my personally developed Focused Growth 12-Metric System — an approach I designed to evaluate companies that combine above-average growth potential with strong financial health.

The system is based entirely on my own definitions, thresholds, and scoring rules for what constitutes a Pass, Average, or Fail. These standards reflect how I personally assess whether a stock fits the Focused Growth investing style — which prioritizes sustainable growth backed by solid fundamentals, not just momentum or hype.

Core Focused Growth Metrics

Alphabet shines in almost every growth category. Revenue growth sits at 13.8%, far above the industry’s 7.6%. EPS growth is even stronger at 19.4% versus a 10% industry average, showing that profits are expanding faster than sales. Its PEG ratio of 1.87 comes in slightly below the industry’s 2.0, signaling reasonable valuation given the growth profile.

On profitability, Alphabet is exceptional: profit margins of 31.1% dwarf the industry’s 12%, and ROE of 34.8% shows world-class capital efficiency. The only soft spot is valuation — the forward P/E of 22.8 is slightly higher than the 22.0 industry average. That’s not extreme, but it does mean expectations are built in.

Scorecard: 5 Pass, 1 Average — excellent growth and profitability, with valuation fair but not cheap.

Quality & Stability Metrics

On stability, Alphabet also looks strong. It generated $49.8B in free cash flow, giving it ample capacity to reinvest or return cash to shareholders. Its market cap of $2.47 trillion ensures resilience through sheer scale. The debt ratio is only 11.5%, far below the 50% caution line, which gives the company flexibility in downturns.

Return on invested capital (ROIC) sits at 16.8%, comfortably above the 12% benchmark that signals efficient use of capital. Insider ownership looks misleadingly low in some datasets — listed as 0% — but in reality, Google’s founders still control significant Class B shares with super-voting rights, anchoring long-term culture and direction. Finally, Alphabet’s moat strength scores 90/100 in my system, reflecting dominance in search, ads, and growing presence in cloud and AI.

Scorecard: 5 Pass, 1 Noteworthy caveat on insider reporting — overall stability remains a core strength.

Overall Score & Investor Takeaway

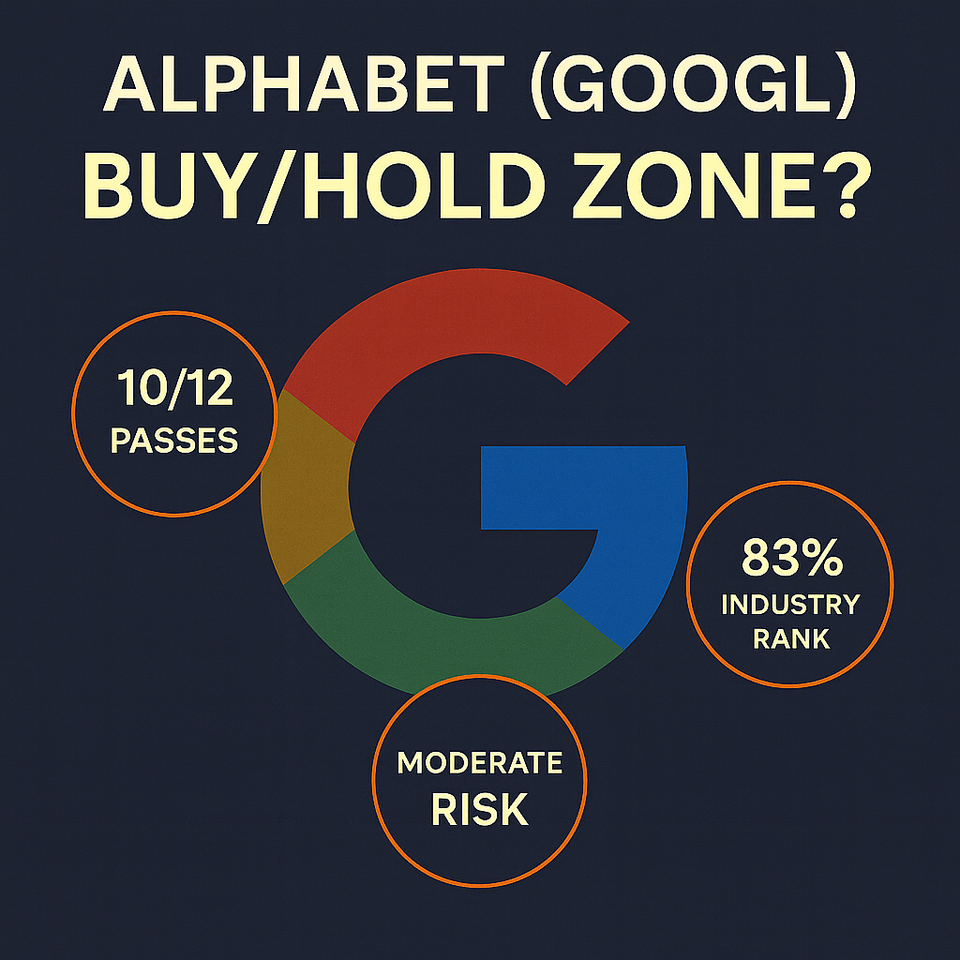

Alphabet passes 10 of 12 metrics in the Focused Growth framework, placing it in the top tier of large-cap tech. With double-digit growth, exceptional margins, and disciplined capital returns, the business fundamentals remain world-class.

The risks are clear:

- Valuation drift: at 22x forward earnings, any earnings miss could trigger multiple compression.

- Regulatory headwinds: antitrust pressures remain real.

- Innovation pipeline: success depends on execution in AI and cloud.

Verdict (Focused Growth Lens): Buy/Hold Zone. Alphabet remains an attractive long-term position, with the best entry points likely coming on market pullbacks.

Methodology Note

The Focused Growth 12-Metric System is my proprietary stock evaluation method. All thresholds, scoring definitions, and interpretations are based on my personal investing style and are not standardized financial metrics. While the data itself is sourced from reliable providers, the scoring reflects my own analysis and judgment.

Disclaimer

This analysis is for informational purposes only and is not financial advice. Always conduct your own due diligence or consult a qualified professional before making investment decisions.

Member discussion