Apple (AAPL): Fortress on Fumes

Originally appeared on Substack at phaetrix.substack.com.

Apple just delivered another “beat” - $102.5B in Q4 revenue, up 8%. Services hit an all-time record at $28.8B, up 15%. Management guided to the “best December quarter ever” with 10-12% growth.

The stock barely moved.

Here’s why: Apple is reportedly nearing a ~$1 billion/year deal to license Google’s Gemini AI to power the next-generation Siri, launching spring 2026. Not because Apple can’t build AI - but because it’s behind. The company that pioneered the smartphone is now paying a search engine company to fix its voice assistant.

Meanwhile, iPhone revenue missed estimates despite “off the chart” demand claims, and China revenue fell 4%. The fortress is intact. The moat is deep. But the growth engine that justified 36× earnings? That’s running on fumes.

FAST Graphs affiliate link: I may earn a commission at no extra cost to you

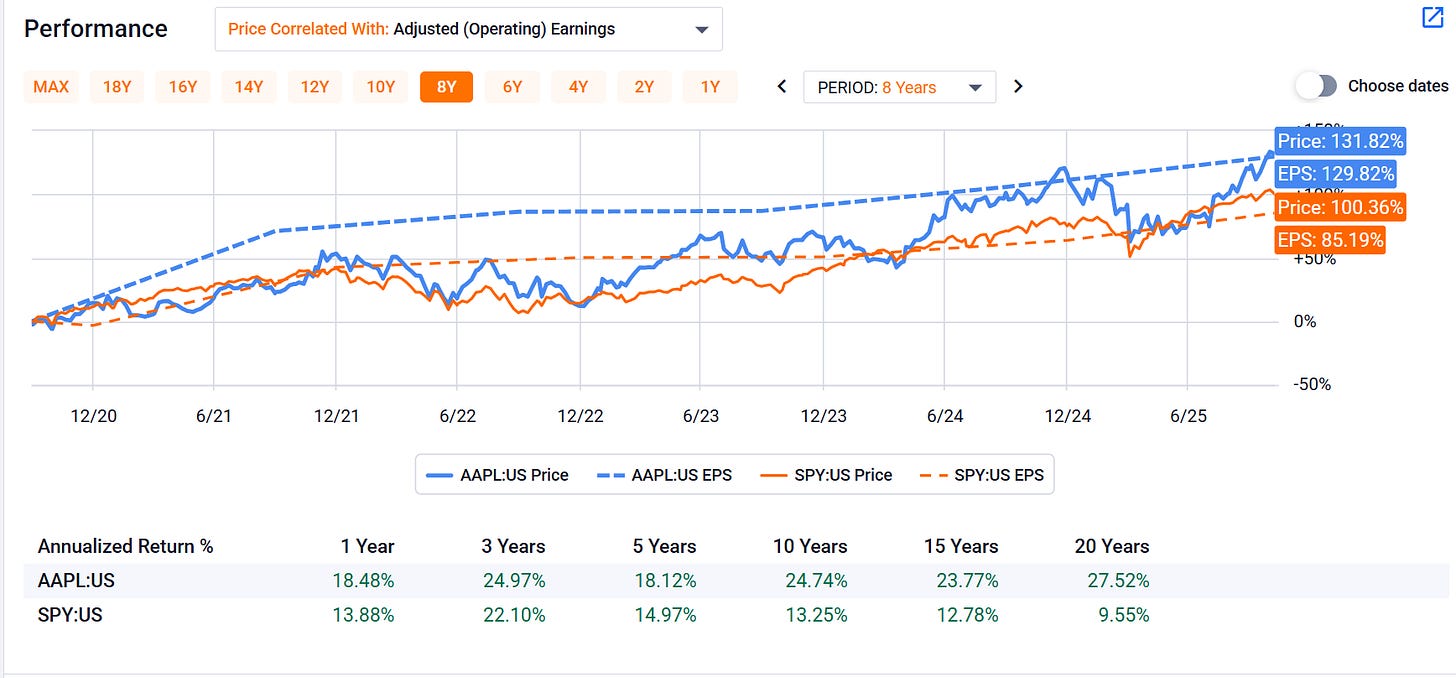

Eight years of outperformance - but notice how price (blue) pulled away from earnings (dashed blue) starting in 2024. That gap? Multiple expansion on slowing growth.

📊 The Scorecard

✓ Moat: A+ — Ecosystem lock-in is unbreakable

✓ Cash Flow: A — $100B+ annual FCF, fortress balance sheet

⚠ Growth: C — 8% revenue growth, iPhone cycles stretching to 3+ years

✗ Valuation: D — 36× earnings for single-digit growth

⚠ Risk Profile: C- — China exposure, tariff headwinds, beta 1.11

✗ Innovation: D+ — Outsourcing AI to Google, refinement over reinvention

🔥 Heat Map: Where’s the Fire?

🟢 Services – Growth engine

→ Watch for: Slowdown below 12% YoY = multiple compression time

🟡 iPhone – Mature but stable

→ Watch for: December quarter miss = “supercycle” narrative dies

🔴 China – Bleeding

→ Watch for: Rebound signal: +2% QoQ for two quarters

🔴 AI Strategy – Playing catch-up

→ Watch for: In-house model launch ahead of late-2026 = game changer

🟡 Valuation – Stretched

→ Watch for: Fair entry: sub-$250 (28× earnings or lower)

The Bull Case: Services + AI = Sustained Premium

Bulls point to Services growing 15% and tracking toward $120B+ annually by 2027-2028. The Gemini partnership buys time while Apple finishes its own AI model. iPhone 17 demand is creating supply constraints, with double-digit revenue growth expected this quarter.

The new iPhone Air form factor, A19 chips, and Liquid Glass UI refinements reinforce ecosystem lock-in - even if these represent refinement, not revolution.

FAST Graphs affiliate link: I may earn a commission at no extra cost to you

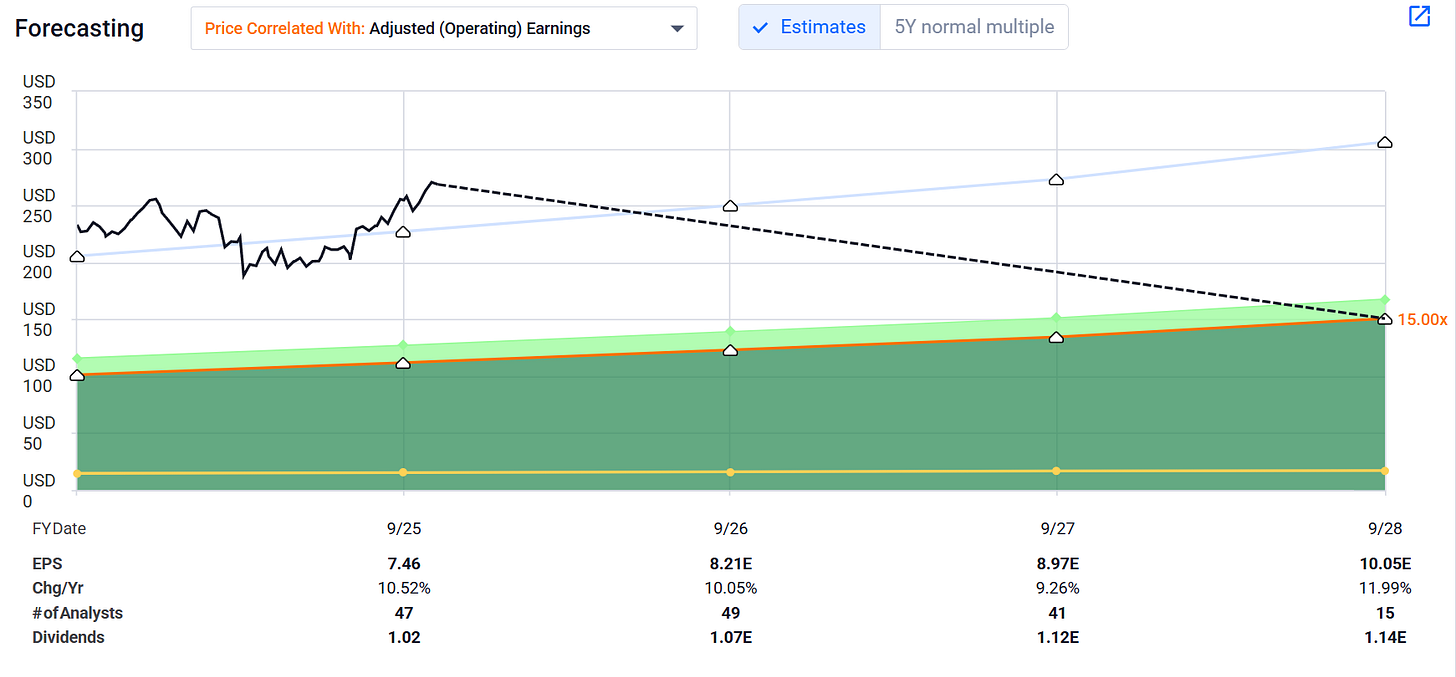

Analysts project 10-12% EPS growth (green line), but price is already running ahead of that trajectory. The widening uncertainty cone tells the real story - nobody’s confident about the AI payoff.

My Take

Apple executes flawlessly on what it already does. But nearly half its incremental growth now comes from pricing power and services expansion, not new categories or accelerating hardware sales. The iPhone franchise - eighteen years old - is durable but mature. Replacement cycles stretch toward 3+ years.

At 36× earnings, Apple needs 10%+ annual revenue growth through 2030 to sustain its multiple. Using a 9% cost of equity in a standard DCF model, I calculate fair value around $240/share (25× earnings) - where fundamentals meet gravity. Current price: $271.

Red Flags

Key risks stacking up:

- Multiple compression if yields stay elevated or Services growth slows

- China/Taiwan exposure - China already down 4%, more downside likely

- Tariff costs ran $1.1B last quarter, with $1.4B expected in the holiday quarter

- App Store fee scrutiny threatening Services margins - regulatory risk is real

Beta sits at 1.11 - a 10% S&P drop means ~12% downside for Apple.

What Would Change My Mind

I’d turn bullish if:

- Services growth accelerates past 20% for two consecutive quarters

- China stabilizes and returns to growth

- Apple’s in-house AI model launches ahead of schedule and actually impresses

- Valuation compresses to 28× or below on the same fundamentals

Until then, I’m watching from the sidelines with a long position I refuse to add to.

Value Math: Fair Value $240

Using conservative assumptions:

- 8% revenue growth through 2027

- Services margin sustained at ≥70% (mid-70s range)

- 9% cost of equity

- Terminal growth 4%

DCF lands at $240/share - an 11% haircut from current levels. That’s where math meets reality, and the premium for “safety” gets properly priced.

FAST Graphs affiliate link: I may earn a commission at no extra cost to you.

The analyst range tells the story: bulls see $300+ (AI supercycle dreams), bears see sub-$200 (multiple collapse), consensus hovers around current levels. My $240 fair value sits where fundamentals meet gravity - not pessimistic, just realistic.

My Kill Switch

I exit if:

- Services growth drops below 10% for two quarters

- FCF yield falls below 3% - cash generation stalls

- China revenue drops another 10%+ - geopolitical risk materializing

Multiple expansion continues past 40× - speculation replacing fundamentals

Bottom Line

Apple mints $100B+ in annual free cash flow and returns most through buybacks and dividends. Wide moat, excellent execution, fortress balance sheet.

But growth has settled into predictability. AI strategy outsourced to Google. iPhone 17 is refinement. China weakening.

Timeless titan. Predictable grind. Priced like the next big thing - but it’s not.

Price Target: $240 | Trading ~$268 (as of Nov 8) | Downside: ~10%

What I’m Watching

- Services momentum vs. regulatory pressure on App Store fees

- December quarter iPhone 17 results - real demand or tariff pull-forward?

- Spring 2026 Gemini-powered Siri launch

Margin expansion trajectory - can Apple push past 50% gross margin?

Disclosure:

Long AAPL position.

Charts:

Analysis powered by [FastGraphs] - the tool I use for every valuation deep dive. Affiliate link - I may earn a commission at no cost to you.

Member discussion