Chevron: Built for Cash, Not Clicks

Chevron (NYSE:CVX) spent two years in arbitration hell over the Hess deal — every analyst calling it a distraction, every bear pointing to the $53 billion price tag. Yet here it is, trading at $153 with free cash flow most tech companies would envy.

At 16.5× forward earnings on 2026 EPS of $9.27, you're paying for discipline, not disruption. Upstream margins hold near 80%, production's climbing 6% annually, and the "post-acquisition overhang" never materialized.

Bulls see Guyana + Permian driving $26 billion free cash flow by 2027; bears point to $70 oil dependency and Tengiz execution risk. I see a cash machine that just locked up one of the world's lowest-cost oil fields while competitors chase shale scraps.

At a $314B market cap and 4.5% yield, Chevron's priced like a survivor — but performing like a compounder. Target: $170 by 2027.

Fundamentals: Free Cash Flow Covers the Dividend 1.7x

Chevron's 2025 numbers: revenue down 8% to $181 billion, with operating EPS at $8.34 — a 17% decline on merger costs. Production? Not EVs, but barrels: 3.4 million boe/d, up 3%, led by Permian's 800,000 boe/d. Full-year 2025 tracks to $20 billion in free cash flow — covering the $12 billion dividend 1.7 times with $8 billion left for buybacks. Bloomberg projects 2026 EPS rebounding 23% to $10.27 as Hess synergies kick in.

Net debt: 16% of capital with an 82% payout ratio — sustainable even when Brent tanks. Beta at 0.81 means 20% less volatility than the market.

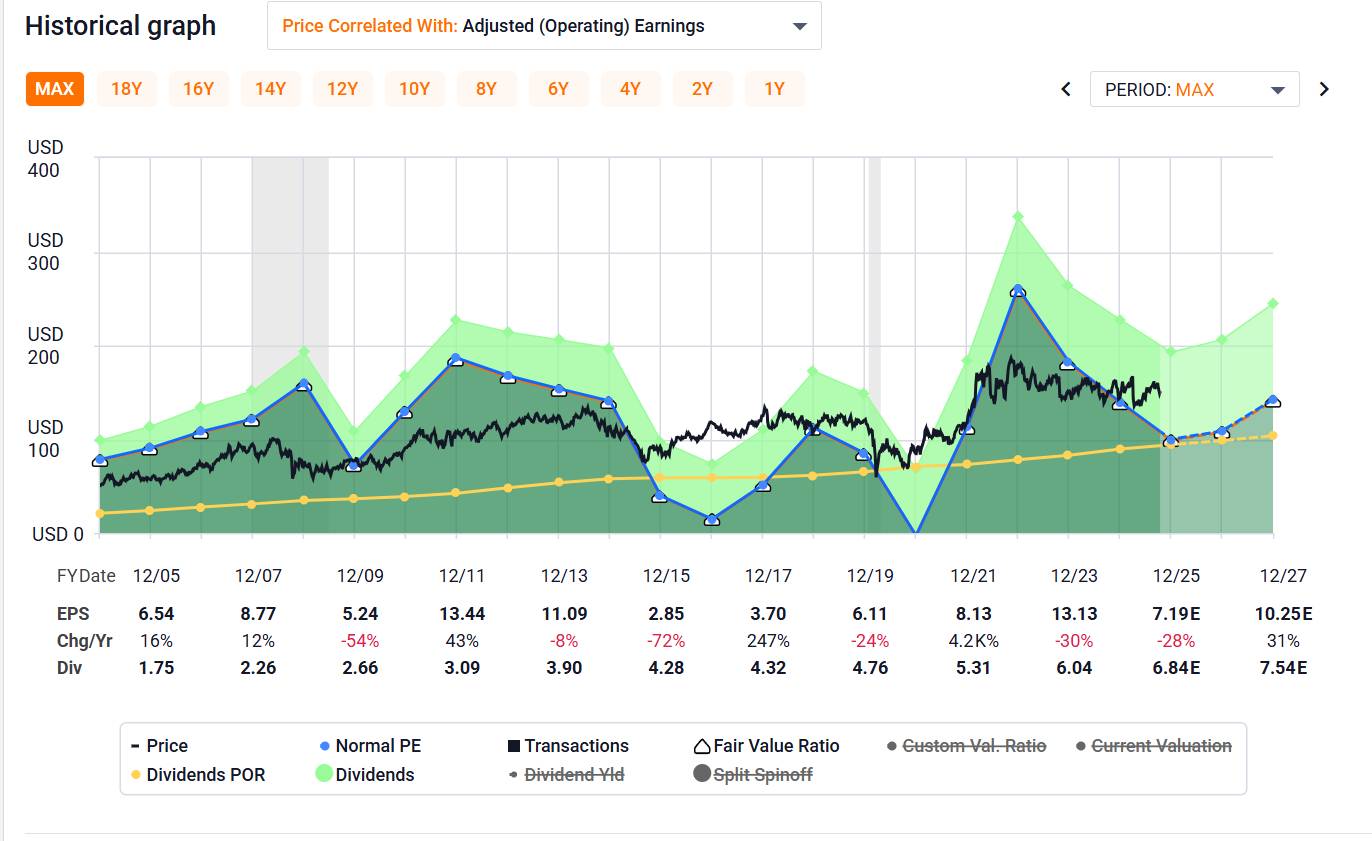

Historical Performance:

(Chart source: FAST Graphs®, © 2025. Used under license for educational commentary.)

Over 20 years, Chevron's earnings swung with oil prices — but dividends never stopped. Not in 2008, 2015, or 2020.

The Bull Case: Scale Wins When Costs Matter

The Hess deal added 30% of Guyana's Stabroek block — breakevens below $35/barrel vs. peer averages above $50, per Morningstar. Chevron now holds 11 billion barrels of reserves with Permian acreage printing cash at $40 oil. Guyana's FPSOs come online by 2028, adding 500,000+ boe/d. Tengiz expansion brings another 260,000 boe/d by 2026. If Brent holds $70-75, free cash flow hits $22-26 billion by 2027 — at 15-17× multiple, that's $170-180 per share.

Dividend? 4.5% yield, up consistently for 38 years. CFRA: "Mid-single-digit FCF growth through 2028 achievable."

My Take: Discipline Beats Narratives

Chevron's edge is capital allocation. Unlike EV subsidies shifting every election, oil demand hit 102 million barrels/day in 2024 per IEA — EVs still under 20% of new car sales globally. Breakevens under $40 (Permian) and $35 (Guyana) mean cash flow stays positive at $60 Brent. Bloomberg's 2027 consensus: $10+ EPS with $22 billion FCF equals $170-180 per share at 17× — right where quality energy trades. Peers like XOM? Exxon's at 13× with worse discipline.

Competition and Execution: Guyana Changes the Math

Chevron's undercutting shale peers at $35 breakevens in Guyana — 600,000 boe/d by 2028. China exposure minimal at 8% revenue. Tengiz is $2 billion over budget but 90% complete, adding 260,000 boe/d high-margin output. This offsets delay risk for steady 5-6% growth.

Bottom Line

Chevron's valuation bets on execution over moonshots. For income investors eyeing predictable cash, this works at $153. My conviction: if Brent stays above $65 and Guyana delivers by 2028, this reprices to $170-180.

What's your take? Can Chevron's Guyana bet justify a 16.5× multiple in a world rotating out of fossil fuels? Share your thoughts below.

Price Target: $165-180 (base case $170)

Disclosure: Long CVX. Not investment advice.

Charts sourced from FAST Graphs® for educational analysis. I'm not affiliated with FAST Graphs. Past performance is not indicative of future results

"I originally shared some of these ideas on Yahoo Finance and explored them further on Substack"

Member discussion