Tesla, Inc. (NASDAQ: TSLA): Priced for Perfection, Delivering Automaker Economics

Tesla is trading at $440 per share with a P/E ratio of 259x based on 2025 consensus earnings of $1.70 per share—investors are paying $259 for every dollar of profit. Meanwhile, automotive margins have compressed from 23% in 2020 to 17.2% today. Bulls point to robotaxis and Full Self-Driving as transformational breakthroughs, while bears see an automaker losing ground to BYD’s sub-$10,000 vehicles.

At a $1.4 trillion valuation, Tesla is priced like it’s already disrupted transportation. The numbers tell a different story—it’s delivering automaker economics with decelerating growth. My target for value-focused investors: $200 per share by 2028, representing significant downside from current levels.

Tesla’s Valuation Problem

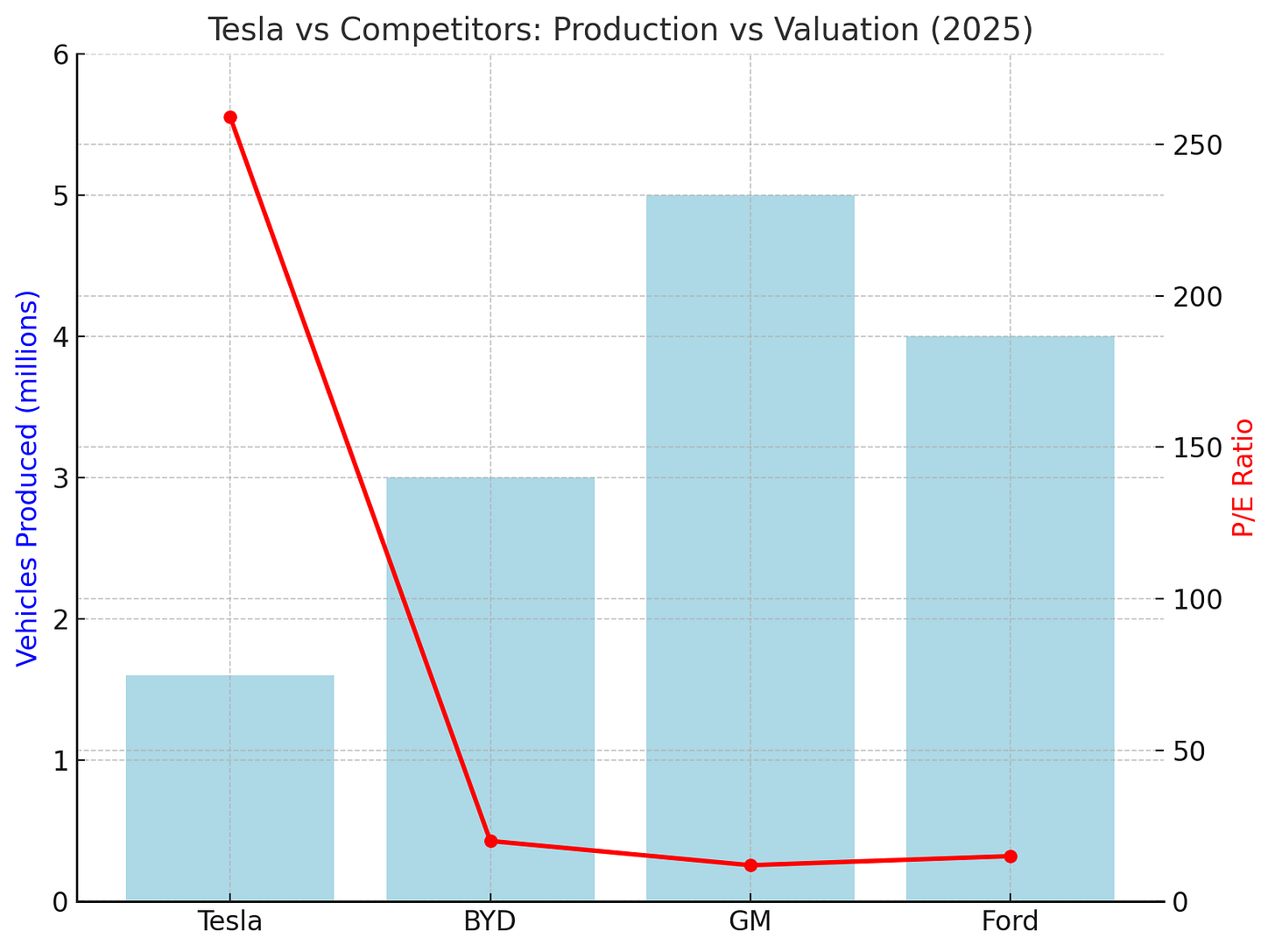

The core issue is simple: Tesla trades at 259x earnings while producing 1.6 million vehicles annually. Compare that to:

- BYD: 3+ million vehicles at 20x P/E

- GM: 5+ million vehicles at 12x P/E

- Ford: 4+ million vehicles at 15x P/E

Tesla commands a 13x premium over BYD despite producing half the vehicles. This premium only makes sense if Tesla transforms into something far beyond an automaker—and soon.

“Tesla is delivering automaker economics at tech multiples. The market is pricing in a future that doesn’t yet exist at scale.”

Growth Has Stalled

Tesla’s Q2 2025 results reveal a company hitting the brakes:

- Revenue fell 12% year-over-year to $22.5 billion

- Automotive revenue declined to $16.7 billion (from $19.9 billion)

- Vehicle deliveries dropped 13.5% to 384,000 units

- EPS came in at $0.40, missing FactSet’s consensus of $0.43

- Free cash flow collapsed 89% to just $0.146 billion

Full-year 2025 is tracking toward $88 billion in revenue based on trailing twelve months, down from $97.7 billion in 2024—Tesla’s first annual revenue decline in over a decade.

Looking ahead, Bloomberg consensus projects 2028 revenue at $90-92 billion, representing just 3% compound annual growth from 2024 levels. For context, Tesla grew revenue at 50%+ annually from 2019-2022. This dramatic deceleration raises fundamental questions about whether Tesla deserves its premium valuation.

Key Metrics Trending Wrong:

- U.S. BEV market share: 48% (down from 79% in 2020)

- 2025 projected deliveries: ~1.6 million vehicles

- 2028 analyst projection: 1.8-2.0 million (modest growth)

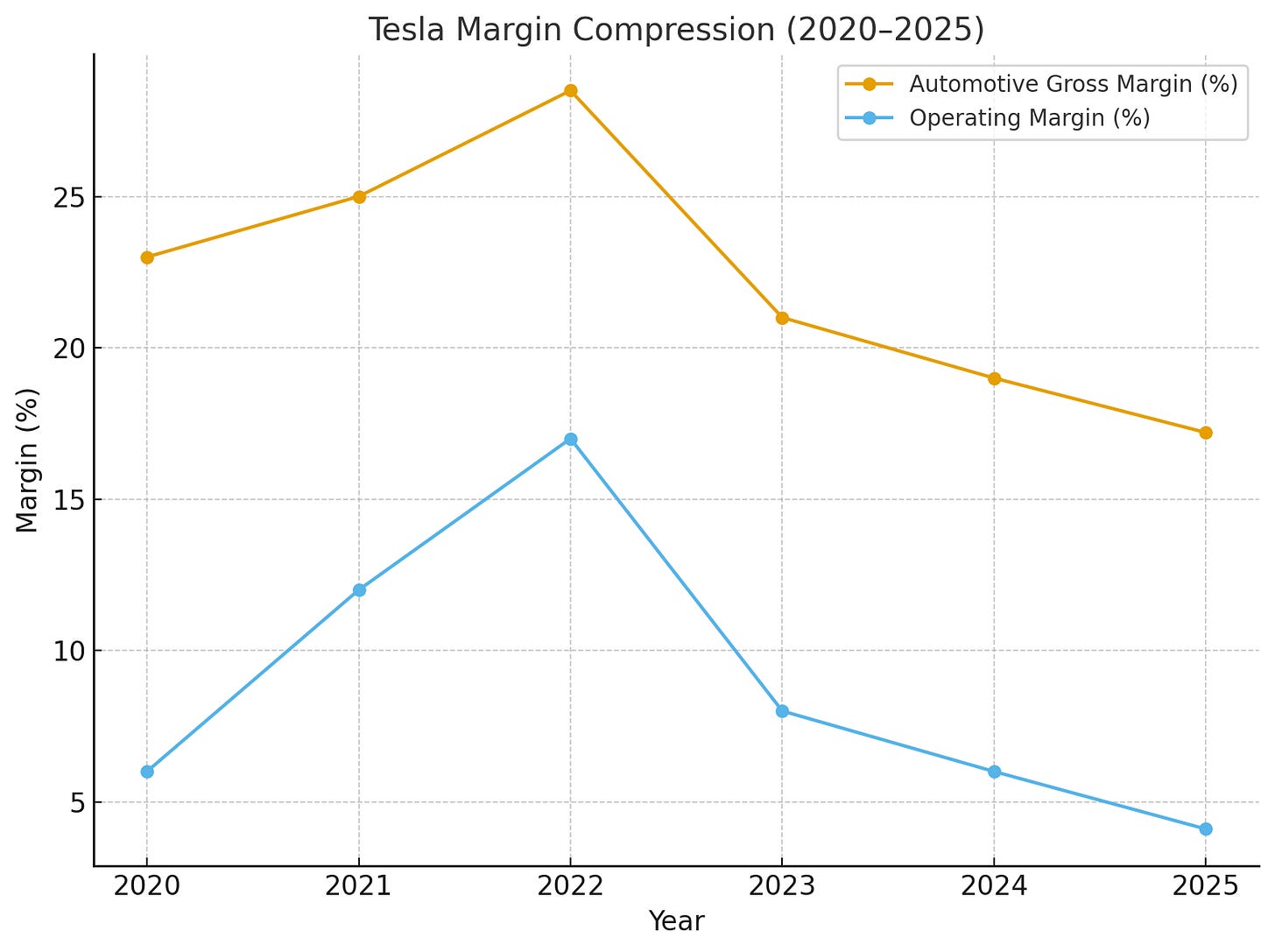

Margins Under Pressure

The margin story is equally concerning:

- Automotive gross margins: 17.2% (down from 23% in 2020 and 28.5% peak in 2022)

- Operating margin: 4.1% (approaching traditional automaker levels)

Chart 2: Tesla Margin Compression (2020-2025)

This isn’t a temporary blip—it’s a structural shift. Competition from BYD and Chinese manufacturers is forcing Tesla into a brutal trade-off: match their prices and kill margins, or maintain pricing and lose volume. Neither option is attractive at current valuations.

“At 4.1% operating margins, Tesla looks less like Apple and more like GM with better software.”

The Bull Case: Why Investors Stay Optimistic

Before diving deeper into my bearish thesis, let’s be intellectually honest about why smart investors remain bullish. Dismissing their arguments would be lazy analysis.

The FSD Data Advantage

Tesla has accumulated over 7 billion Full Self-Driving miles according to the company’s Q2 2025 update, with roughly 1 billion miles added annually. This dwarfs Waymo’s 22 million urban miles—Tesla has 300x more data than Waymo.

Bulls argue this data moat is Tesla’s secret weapon. Every mile driven generates training data that improves the neural network. As more vehicles join the fleet and FSD adoption increases, the data flywheel accelerates. If Tesla translates this advantage into Level 4 autonomy ahead of competitors, the payoff could be enormous.

Robotaxi Revenue Potential

Ark Invest’s 2025 research projects that robotaxis could generate $1 trillion in annual revenue industry-wide by 2030 if true autonomy is achieved. If Tesla captures even 20-30% of this market, we’re talking about $200-300 billion in high-margin revenue—enough to completely transform the company’s economics.

The Austin robotaxi pilot launched in June 2025 with safety drivers, marking Tesla’s transition from concept to execution. Bulls see this as proof that commercial deployment is imminent, not theoretical. If Tesla scales this service to major metros over the next 2-3 years, revenue could reach $10-20 billion annually by 2028.

Energy Storage: The Hidden Growth Engine

While automotive grabs headlines, Tesla’s energy storage business quietly grew 100% year-over-year in 2024 according to company filings. Megapack deployments are accelerating globally as utilities seek grid-scale battery storage.

Bulls point out that energy storage carries higher margins than automotive (20%+ vs. 17.2%) and faces less competition. If this business reaches $15-20 billion in annual revenue by 2028 with 20%+ margins, it adds $3-4 billion in operating income—meaningful contribution to overall profitability.

The Bull Scenario: $500-600 Per Share

If FSD achieves Level 4 regulatory approval in multiple states by 2027, robotaxis scale to $10+ billion in revenue by 2028, energy reaches $15+ billion with strong margins, and automotive stabilizes at 1.8-2.0 million deliveries with 18%+ margins, Tesla could generate $12-16 billion in net income by 2028. At a 30-40x multiple (reasonable for a high-growth tech platform), that yields $500-600+ per share.

Bulls aren’t crazy—they’re betting on a specific set of outcomes that are possible, if challenging to achieve.

My Counter: Data Doesn’t Equal Regulatory Approval

I’ve studied the bull case carefully, and I respect the logic. Tesla’s FSD data advantage is real, and the robotaxi opportunity is massive if it materializes. However, bulls are underestimating three critical risks:

Regulatory Reality Check

Tesla’s 7 billion FSD miles are impressive, but regulatory approval doesn’t depend solely on technical capability—it depends on government agencies comfortable with public safety implications. NHTSA oversight, state-by-state approval processes, insurance framework development, and liability questions create 2-3 years of uncertainty at minimum.

Even Waymo, with fewer miles but more controlled urban testing, has faced regulatory delays in expanding beyond limited geographic areas. Tesla’s approach—deploying FSD to millions of consumer vehicles nationwide—faces even more scrutiny because it involves public roads with minimal geographic constraints.

“Data scale is necessary but not sufficient. Regulatory approval depends on politics, public perception, and risk tolerance—none of which Tesla controls.”

My base case: FSD achieves limited Level 4 approval in 1-2 states by 2027, with broader rollout delayed to 2029-2030. This timeline means robotaxi revenue reaches only $3-5 billion by 2028, far short of the $10-20 billion bulls expect.

Competition: The BYD Threat

Chart 1: Tesla vs Competitors - Valuation & Production

Tesla’s cost per vehicle sits around $36,000 for its 1.6 million annual production—better than GM and Ford at $45-50,000, but BYD hits $30,000 for comparable EVs like the Seagull, with entry models under $10,000. BYD produced over 3 million vehicles in 2024 per company reports—nearly double Tesla’s output.

China represents roughly $20 billion of Tesla’s annual revenue (about 22% of total), and this is now under direct assault. BYD’s domestic dominance in China is absolute, and they’re expanding aggressively into Europe and Southeast Asia.

In the U.S., Tesla’s BEV market share has plummeted from 79% in 2020 to 48% in 2025 as legacy automakers (GM, Ford, Hyundai) and new entrants (Rivian, Lucid) flood the market. Pricing power has evaporated—Tesla has cut prices repeatedly to maintain volume, directly impacting margins.

Musk’s Divided Attention

Elon Musk now splits time between Tesla, SpaceX, X (Twitter), xAI, Neuralink, and government advisory roles. Multiple reports suggest FSD development has slowed as engineering resources shift to xAI projects. If FSD deployment slips 6-12 months due to resource constraints, that could reduce 2026-2027 earnings by $0.50-$1.00 per share according to analyst models.

Valuation Reality

Strip away the robotaxi dreams, and Tesla is an automaker. Based on Bloomberg’s 2028 revenue consensus of $90-92 billion and my estimated $5-6 billion in net income (assuming 6-8% net margins if robotaxis underperform), Tesla generates profitability similar to traditional automakers.

If we apply a 9-10x P/E multiple to my estimated $8-9 billion in normalized net income (assuming modest robotaxi contribution), Tesla’s fair value is $160-240 per share. Even using a generous 20x multiple (acknowledging energy growth and FSD optionality), we get $300-350 per share.

“The current $440 price implies investors are paying for transformational outcomes that don’t yet exist at scale.”

Scenarios: Bear, Base, Bull

Bear Case: $160-200 Per Share

- Robotaxi deployment stalls beyond 2028 due to regulatory delays

- Automotive margins compress to 14-15% as competition intensifies

- BYD and Chinese competitors capture additional market share

- 2028 net income: $6-8 billion

- Valuation: 10x P/E (automaker multiple)

- Price Target: $160-200

Base Case: $300-400 Per Share

- Limited robotaxi revenue ($3-5 billion by 2028)

- Automotive margins stabilize at 16-17%

- Energy contributes $5-8 billion in revenue with strong margins

- 2028 net income: $10-12 billion

- Valuation: 20-25x P/E (hybrid auto/tech multiple)

- Price Target: $300-400

Bull Case: $500-600 Per Share

- FSD Level 4 broadly approved by 2027

- Robotaxis generate $10+ billion revenue by 2028

- Energy scales to $15+ billion with 20% margins

- Automotive margins recover to 18-19%

- 2028 net income: $14-18 billion

- Valuation: 30-35x P/E (tech platform multiple)

- Price Target: $500-600

What Would Change My Mind?

I’m bearish, but I’m not dogmatic. Here are the milestones that would make me reconsider:

Bullish Indicators (2026-2027):

- FSD Level 4 regulatory approval in 2+ major states (California, Texas, Florida)

- Robotaxi revenue reaching $1+ billion quarterly by Q4 2026

- Automotive gross margins stabilizing above 18%

- Energy revenue exceeding $3 billion quarterly with 20%+ margins

- Q4 2025 or Q1 2026 deliveries exceeding 500,000 units

Reassessment Triggers:

- Stock price falling below $300 with FCF consistently above $2 billion quarterly

- Clear regulatory pathway for nationwide FSD deployment

- Evidence of sustainable competitive advantages against BYD in China

If Tesla hits these milestones, I’ll revisit my thesis. Good investors change their minds when the facts change.

Bottom Line

Tesla’s $1.4 trillion valuation assumes transformational outcomes that may or may not materialize. Bulls betting on robotaxis and autonomy breakthroughs could be proven right—the technology is advancing, and the addressable market is enormous.

However, for value investors focused on current fundamentals, the risk-reward is deeply unfavorable at $440 per share. You’re paying for a future that doesn’t exist yet, while the core automotive business faces margin compression, market share erosion, and intensifying competition.

“Tesla will remain a major player in EVs and energy storage. But at automaker valuations (10-20x earnings), not tech platform multiples (40-60x earnings).”

My conviction: Without $5+ billion in robotaxi revenue by 2027 and clear regulatory pathways to nationwide deployment, Tesla reprices significantly lower as investors recalibrate expectations.

For growth investors: If you believe FSD achieves Level 4 approval in the next 18-24 months and robotaxis scale rapidly, Tesla could justify $500-600. This is a binary bet—you’re either right and make 30-40%, or wrong and lose 40-50%.

For value investors: Avoid at these levels. Wait for either: (1) price below $300 with improving fundamentals, or (2) clear evidence that robotaxis are scaling with regulatory approval.

Price Target: $160-240 per share (base case $200)

Join the Debate

Tesla bulls: convince me I’m wrong. Does the robotaxi vision truly justify $440 today? Drop your take below—the best debates sharpen all of us.

If you found this analysis useful, share it with someone wrestling with Tesla. And if you think I’ve missed something critical, tell me why in the comments.

For more contrarian investing analysis, check out:

- Income Investing: The Guide to Building A Cash Flow Engine

- Building a Dividend Portfolio That Actually Works

Disclosure: No TSLA position at time of publication. This analysis is for informational purposes and does not constitute investment advice. Always conduct your own due diligence and consult with a financial advisor before making investment decisions.

Originally published on Phaetrix Substack on October 4, 2025.

Member discussion